A few longer-run trends continue to dominate the supply-side story of cattle in South Dakota. Beef cow numbers continue to decline. The number of feeder cattle outside of feedlots has remained stable. Some inputs remain stable relative to the higher observed cattle prices. These aspects are considered below as they are either directly or indirectly related to the sources of calves.

Earlier in 2026, the National Agricultural Statistics Service (NASS) released cattle inventory estimates with breakdowns at the state level. There were some minor revisions to the 2025 estimates also. The total inventory level for South Dakota was revised slightly lower, mainly among heavy steers and among calves.

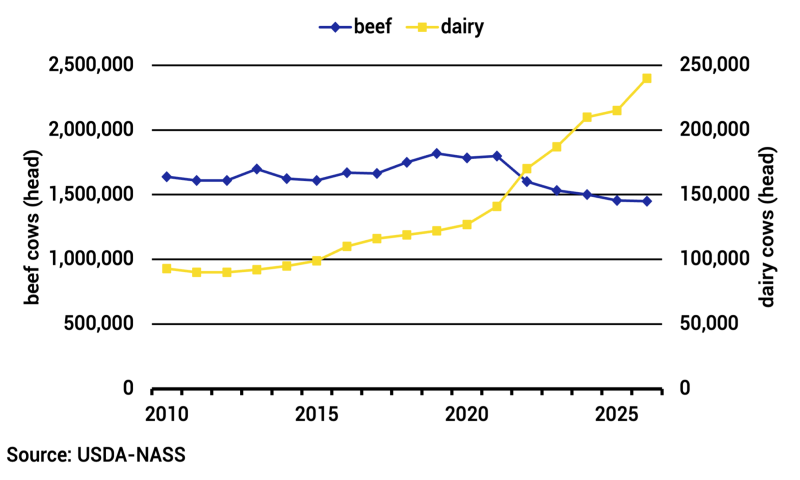

One trend that has not changed in recent years has been a continued slow decline in the number of beef cows that have calved (Figure 1). During the early 2010s, beef cow numbers declined at the national level but had been steady in South Dakota. Since 2021, the number of beef cows in South Dakota has declined, reaching a total last seen in 1977 following a severe drought. Fewer cows mean fewer calves. Since 2021 in South Dakota, the decline in beef cows has been partially offset by a sharp expansion in dairy cows. Historically, the number of beef cows was more than ten times the number of dairy cows. Although calves from dairy cows are becoming more prevalent, they still represent a small share of the overall number of calves.

The number of cattle on feed has been constant for the past decade. As of January 1, 2026, the number on feed was 435,000 head in South Dakota. Large feedlots, those with more than 1,000 head, had a total inventory of 230,000 head. Small feedlots had a total inventory of 205,000 head. The absolute decline in beef cow numbers has been reflected in smaller calf crops, especially in recent years.

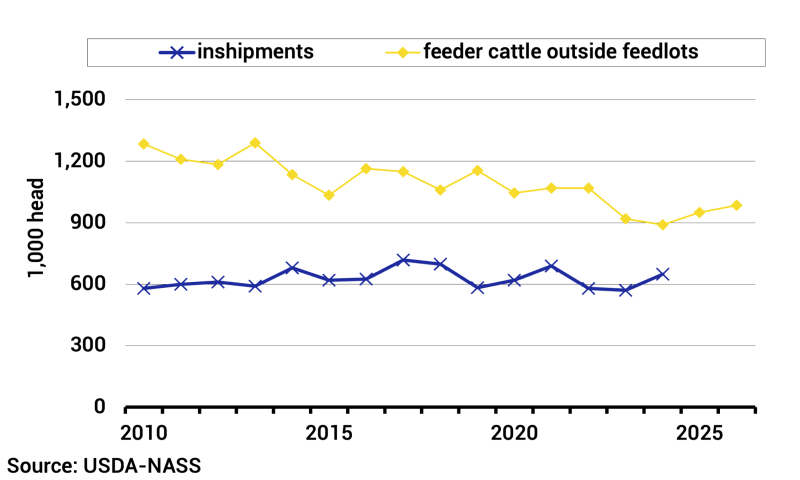

The number of feeder cattle outside of feedlots has been increasing slightly for the past two years (Figure 2). That tally combines the number of non-replacement heifers, steers weighing more than 500 pounds, and calves weighing less than 500 pounds. The number on feed is subtracted, leaving a residual total outside of feedlots. Different cow types explain a little of the recent growth. The increase in dairy cows exceeded the decrease in beef cows from 2025 to 2026. Heavier weights, or adding more weight to existing animals, may be another factor. If a feedlot or backgrounding operation feeds animals longer, then those animals will remain in inventory for a longer time. Slaughter weights, for example, have continued to get heavier at the national level.

Another source of calves and feeder cattle are inshipments. These are the net level of cattle brought into the state, estimated annually by NASS, mainly from state-level sources. For example, some calves from western states may be bought by feedlots in South Dakota. Some calves from South Dakota are bought by feedlots in southern states. The level of inshipments has been steady, suggesting calves from other locations continue to flow into South Dakota (Figure 2). The lagged nature of this measure, the 2025 total will not be released until late April 2026, is a limitation for decision making.

Calf and feeder cattle values reflect parts of the fed cattle supply chain. Corn and hay prices have fallen after better production has eased supply pressure. Receiving a little less attention is the price for pasture and forage. Pasture rent from NASS for South Dakota fell slightly in 2025 to $31.00 per acre. The grazing fee rate from NASS for South Dakota on an animal unit month basis was up slightly in 2025 to $36.50. Fewer beef cows would mean less demand for grazing, putting downward pressure on fees. Low grazing costs, in turn, could facilitate cowherd expansion or running yearlings on grass.